Things can only get better? How to prevent 5 more years of living standards stagnation

On this page

- Introduction

- People's financial resilience has never been lower

- Here are 3 ways the government can make sure people are more shock-proof to future crises:

- 1. Support people with their biggest and most volatile costs - rent and energy

- 2. Make sure people can benefit properly from growth - by ensuring better quality employment

- 3. Don't erode the resilience of those who are already most at risk - including disabled people and families with children

- Building resilience long-term will also rely on access to impartial, expert advice

- Endnotes

Acknowledgements

This report was written by Julia Hamilton, Meri Åhlberg and Emer Sheehy, with input and support from Laura Hutchinson, Eva Souchet, Lutfor Rahman, Daniel Haigh and many others.

Introduction

It’s been 5 years since the first COVID-19 restrictions came in, which caused many businesses to close, and millions of people to be furloughed.[1] Since, it’s been 5 years of repeated challenges for our clients. After the economic shock of lockdowns, we faced spiralling energy prices and inflation spiked at 11.2% in 2022[2] - and we've seen more people come to us with issues related to the cost of living than ever before.

While these peaks have now come down, many are still grappling with the fallout. The pandemic showed how important it is for a society - and households - to be financially resilient to unexpected shocks. While many things have changed in the last 5 years - including the government - much of the economic context has not. Uncertainty driven by global events and tight fiscal rules leaving the government little wiggle room also point to a bumpy road ahead.

In this report, we explore how resilient people will be to future shocks. To do this, we have compared the finances of the people we helped with debt advice in 2019 and 2024,[3] and conducted nationally representative polling.[4] We found that for the people we help - and the country at large - the next economic shock will hit even harder than those of the last 5 years.

People's financial resilience has never been lower

Through our specialist debt advice, we can track incomes and costs in real time for the thousands of people we help with debt each year - up to 85,000 last year.[5] We found that, for the people we help with debt, income has increased by a third on average over the past 5 years - but all of it and more has been eaten up by rising essential costs. While income has gone up by roughly £410 on average, expenditure has gone up by £420.

So it comes as no surprise that nearly half of the people we helped with debt last year were in a negative budget (where their income is not enough to cover their essential costs, even after they have been supported to set a sustainable budget by a debt adviser) - up from 37% in 2019.[6] Expenditure continuously outpacing income rises has meant our clients have gone from treading water, with an average of £21 left over each month after essentials in 2019, to being in the red with an average deficit of -£13 each month last year. This means they have no means of repaying their debts, or any buffer if costs were to rise again.

Half a decade of living on empty has impacted everyone. Among the people we help, even those working full time have seen rises in their essential expenditure outpace rises in their incomes.[7] Our new research covering people across the UK found that over a quarter of people are struggling to cover their essentials each month. Many are turning to desperate measures to pay their bills, with nearly a third using credit and just under half using savings. And this is all before next month’s scheduled price hikes hit - over a third of the people we asked said they’re going to find it difficult to afford a £20 increase in their essential bills, with a quarter telling us they would have to use savings to pay for them.[8] Looking at our debt clients, an expenditure increase of just £20 will push 13% of those still in a budget surplus into the red.[9]

As a result, many have fallen behind on their bills and borrowed money to keep up with rising costs - driving more and more people into debt. Last year, we helped nearly 400,000 people across England and Wales with debt - our busiest year yet for debt advice. In January we helped over 50,000 in one month - a record high. Though the amount of debt people were in on average fell during the pandemic, it’s risen by nearly a third since 2022 due to the cost of living, and is now 10% higher than in 2019 - now at over £8,200 per person.[10]

All of this means people have never been less prepared for another economic shock - nearly a third of people we asked told us they’re less prepared for another financial shock than they were 5 years ago.

The government has committed to improving living standards in all parts of the UK, as part of their mission to grow the economy.[11] But much of the focus has been on growth and moving people into work, which misses the full picture. It fails to account for the ongoing rise in living costs, which have chipped away at people’s buffer, and could swallow up any future increases in income.

At the same time, we know that the tight fiscal rules set by the government mean that cuts to benefits are likely, particularly for disabled people.[12] This risks further damaging resilience for those most at risk, and could undermine wider efforts to improve living standards through growth, and initiatives like the Child Poverty Strategy.[13] The government urgently needs to help people strengthen their foundations, so that they can weather bumps in the road towards growth in the coming years.

Here are 3 ways the government can make sure people are more shock-proof to future crises:

1. Support people with their biggest and most volatile costs - rent and energy

The two biggest expenses for the people we help are still rent and energy. Even if and when incomes rise, people are at risk of all their extra money being eaten up by these essentials - as has been the case for the past 5 years. Taking on extra shifts or second jobs cannot be the answer to the issue of spiralling costs.

Among the people we helped with debt advice last year, private renters spent half of their income on rent and energy alone. And rents continue to tick up - the average proportion of income our debt clients spend on rent has risen from 38% in 2019 to 41% last year, despite increases in income. It comes as no surprise then that, in the past 5 years, private renters have gone from treading water to being nearly £50 in the red.

Private renters do their best to keep a roof over their heads, but with limited options. They juggle bills, paying water one month, electricity the next, because they can't afford everything. Whether working or on benefits, their income just isn’t enough.

Last year’s uprating of Local Housing Allowance (LHA) - which determines the amount of benefits income private renters can get to help with their rent costs - was welcome, but came after four years of freezes. Policy makers would be mistaken in thinking this was sufficient. LHA is now frozen again, despite people facing continuous bill hikes across the board - rents were up 8.7% in the 12 months to January of this year, continuing a trend of high rental inflation that started in the summer of 2021.[15]

While the government is putting in plans to build more social housing, which should reduce the need for people on low-incomes to pay high private rents, this will take years to deliver. In the meantime, shortfalls between LHA and rents will continue to cause problems, for both renters and the government. Families with rent shortfalls that can’t be covered by their income (from benefits or work) are often forced to rely on crisis support like the Household Support Fund or Discretionary Housing Payments. Those who can’t access support to make up the shortfall risk being evicted, with many being made homeless, increasing demand for temporary accommodation.[16] Increasing LHA is the best lever available to the government to immediately mitigate the impact of high housing costs.

LHA must be uprated to the 30th percentile permanently, to provide the safety net people need while longer-term solutions to the housing crisis are put in place.

Energy remains a big issue for our clients - in January it was the most common issue we supported people with.[17] Despite the energy price cap coming down last year, we still supported nearly 100,000 people with energy debts - more than double the number in 2019. Energy debt amounts have also risen by 69% - up from an average of £835 per person to over £1400 last year, far outpacing the 10% average debt increase.[18]

Energy prices are extremely vulnerable to external shocks. The energy price cap, despite being lower than 2022 levels, continues to creep up. From next month people are expected to pay an average of over £100 extra per year on energy, and prices are expected to remain volatile for years to come.[19]

The government’s new Warm Home Discount proposals will extend the £150 support available to households on means-tested benefits.[20] We welcome the news that the support will reach more people - but this won’t be enough. The support available hasn’t kept pace with rising bills - in 2014 when Warm Home Discount was introduced it was worth 12.5% of the average bill, but under the current price cap it makes up just over 8%.[21]

The Government should further reform the Warm Home Discount, providing tiered payments which provide more support to those with highest energy costs.

2. Make sure people can benefit properly from growth - by ensuring better quality employment

Any growth the government pursues needs to be inclusive if it is to achieve their milestone on living standards. One of the government’s big objectives is to increase incomes by moving more people into work. But whether this will improve peoples’ resilience will depend on levels and security of pay, and whether the work provides people with protections when needed.

Currently, for people we see, being in work isn’t a guarantee of financial resilience. The share of full-time workers we help with debt issues who are in a negative budget went up by 40% between 2019 and 2024. Though their income has increased on average by £522 per month in this time, essential spending has gone up by £528, leaving people on average worse off compared to 5 years ago.

On a national level, 1 in 4 of the workers we surveyed told us they were struggling to pay for their essentials every month - and a third told us they’re going to find next month’s price rises tricky. Even among those whose incomes had gone up in the last few years, just under 3 in 10 told us they feel less prepared for another financial shock than they were 5 years ago.

The government is looking to drive up standards in work through the Employment Rights Bill and by increasing the National Minimum Wage, but without proper enforcement, neither change will be effective. Currently, too many of our clients are simply not getting the money they’re owed from work,[22] and are struggling to get redress due to an overburdened Employment Tribunal system and a splintered and underresourced state enforcement system.[23] The government has promised to reform state enforcement through a new Fair Work Agency. This is positive, but will only be effective if it's sufficiently resourced and designed to deliver for those in low paid and insecure jobs.[24]

The government must enforce employment rights through a well-resourced and well-designed Fair Work Agency, to ensure workers are paid what they’re owed.

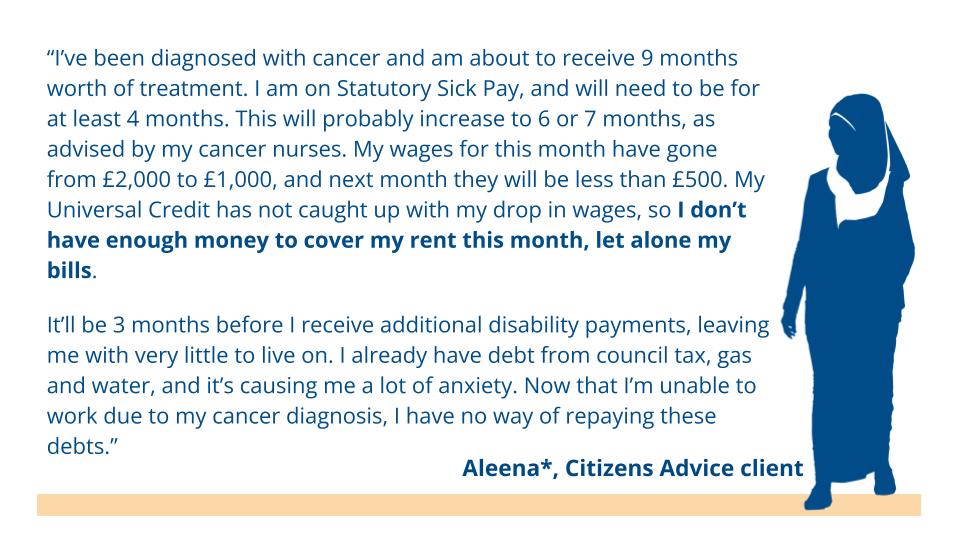

We can also see that employment isn’t providing people with the protections they need. The single largest employment issue we help people with is Statutory Sick Pay (SSP) - the minimum amount employers have to pay their staff who are too ill to work.[25] At only £117 per week, SSP is simply not enough for most to live on. Of the people we helped with SSP in 2023/24, 1 in 5 needed access to charitable support like foodbanks. Even with the government’s promised reforms[26] 9 in 10 of the people we help with debt advice would see their household pushed into a negative budget if they had to rely on SSP for 4 weeks.[27] The rate of SSP needs to increase so people are protected against hardship when they’re at their most vulnerable, and not forced to work through illness and injury to stay afloat.

The government must increase the rate of Statutory Sick Pay to better reflect the National Minimum Wage.

3. Don't erode the resilience of those who are already most at risk - including disabled people and families with children

At the same time, the government needs to recognise that not everyone will be able to earn enough to cover their essential costs. The benefits system needs to offer a proper safety net for when people can’t work or are on low incomes - but successive governments have reduced the value of benefits over many years. Now, the amount people receive in benefits no longer bears any relationship to the actual cost of living.

I think much more recently, within the last three or four years, we are seeing many more mental health clients that have been on long term benefits - but because of the rising price of everything they’re not able to survive on those benefits anymore

The Household Support Fund (HSF) was initially introduced as a short-term response to help people during the cost of living crisis. The government has extended it until next year, which is welcome news. However, crisis support was once a regular part of our welfare system, through local welfare assistance - it should become a permanent fixture again, to help rebuild resilience. All households are at risk of sudden shocks to their income - when people deal with a financial emergency, they need a safety net to prevent crises from escalating.

Because of overall benefit inadequacy, however, many people have been relying on the Household Support Fund for day-to-day spending. In fact, in 2023-24, 39% of the HSF was used to provide free school meals during school holidays - a predictable and routine need that should be met through wider welfare provision.[28] The benefits system should be enabling people to meet these costs so they don’t have to turn to crisis schemes to make ends meet - and so crisis schemes can be reserved for people facing financial shocks.

The government must establish a permanent crisis fund when the Household Support Fund ends next year, and work to reestablish an adequate benefits system to ensure people can comfortably afford the essentials with their income.

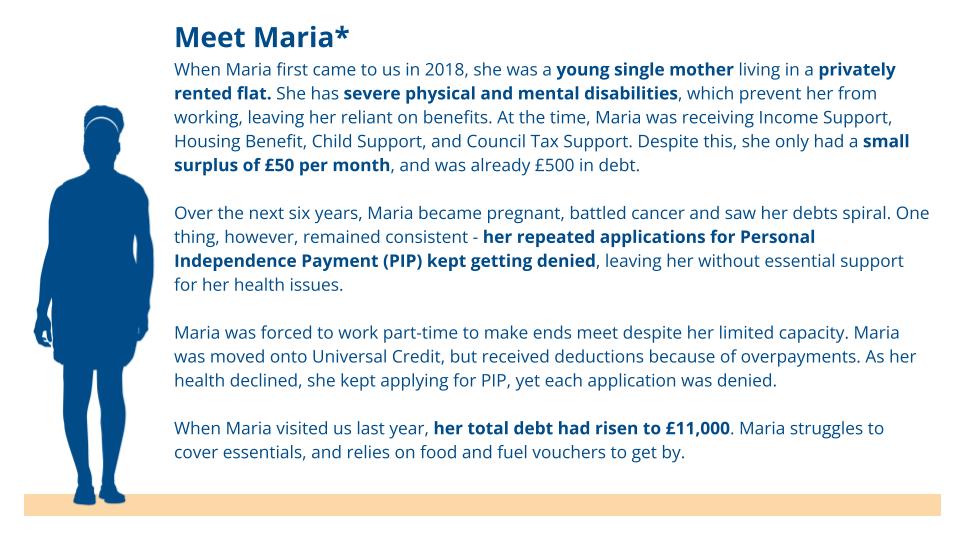

Our data shows that disabled people are some of the most exposed to financial shocks - nearly two thirds (60%) of the people we helped with the HSF in 2024 were disabled or have a long-term health condition.[29] Disabled people who aren’t receiving specific disability benefits, such as Personal Independent Payment (PIP), are some of our worst off clients.

Those who do receive PIP are doing better - but we know from advisers that, increasingly, people are being forced to use their PIP not for necessary medical expenses, but for basic living costs.

That bit of money [PIP] is not used for disability, it’s just used to survive at the moment.

When we polled people receiving disability benefits about their experiences this month, over 4 in 10 told us they were struggling to afford their essentials each month, with half of them using savings, 1 in 4 avoiding medical costs, and 3 in 10 skipping meals to pay their bills.

When people lose PIP, for example because of a reassessment, each month they cut back on spending on health and care by an average of over £200, and spend an average of £130 less on food - actions which likely lead to worsening health outcomes.[30]

The government clearly needs to do more to support disabled people. Instead, they’ve promised to reduce the cost of health and disability benefits - likely through making it harder for disabled people to get the support they need, and reducing the amount of money they receive, further eroding an already at-risk group’s resilience. In an effort to push more people into work, these plans are just going to push more people into poverty.

The government must reconsider disability benefit reform, and instead look at the real barriers people face to accessing work - like the rising levels of poor health, and barriers for disabled people in the job market.

We’ve also been helping more households with children with debt than ever before. Last year we saw double the number of people with children needing specialist debt advice than we did in 2019 - and the number of single parents rose even more at 122%.[31] It therefore comes as no surprise that just under half of everyone that we helped with the Household Support Fund last year was from a household with children - and 1 in 3 were single parents.

Last year, the government set out an ambition to deliver a strategy to reduce the number of children living in poverty in the UK,[32] which currently stands at over 4 million.[33] The strategy is due to report in spring, but change can’t come soon enough for many of the families we help. Ahead of next month’s bill increases, a third of households with children told us they’re already struggling to cover the essentials every month. Over 4 in 10 told us they’ll find it difficult to afford a £20 increase in essential costs - rising to nearly half of single parents. Families are being forced to make tough decisions to make ends meet - a quarter of single parents expect to have to skip meals to manage this increase.

The Child Poverty Strategy offers a huge opportunity to provide more support to families so they don’t continue to face these impossible choices. But the government risks missing this chance if they fail to invest. Providing support with key costs - as highlighted above - will be fundamental to lifting children out of poverty. Housing costs in particular are a huge problem for families with children, with high rents pushing many into unsuitable housing that has detrimental impacts on children’s health, wellbeing, and educational attainment. Providing more consistent support with costs directly affecting parents - including childcare support, and Free School Meals and other schemes to support low income parents with the cost of food - should also be key pillars of the strategy.

But crucially, the government must go further and invest directly in lifting children out of poverty by abolishing the 2-child limit within Universal Credit, and the benefit cap, which disproportionately impact larger families, and single parent households.[34] Analysis of our budget planner data shows that families with children have faced huge increases in key costs over the last five years. Rent and childcare costs have increased by nearly a third, and energy by 50%. Having their income capped by the 2-child limit and/or the benefit cap leaves these families with no means to absorb rising costs. Action here would be the single most targeted way to reduce child poverty.

There is also a serious risk that the government's attempts to make savings on disability benefits undermine their efforts to reduce child poverty. In the past year, nearly a third (29%) of the people we’ve helped with PIP have had dependent children.[35]

The government must urgently publish their Child Poverty Strategy, which should look holistically at how to meaningfully increase incomes and lower costs for families with children.

Building resilience long-term will also rely on access to impartial, expert advice

The aftermath of the last 5 years is still being felt by the people we support, but it’s also being felt across our service. For millions - whether facing a global event or shock, or trying to navigate life events or policy changes - advice is a lifeline. The need for advice has spiked in the 5 years since the pandemic - the number of clients coming to us with issues relating to the cost of living has gone up by 79%, with charitable support and food bank referrals up a huge 187% since 2019.[36]

As well as being an immediate lifeline, access to expert and impartial advice plays an essential role in raising living standards and building financial resilience. Our network of 240 local offices can help people into jobs, stay in work and build financial stability. In solving someone’s problem with Universal Credit or debt, and allowing them to move forward with their lives, our advice can help people improve their health and employment prospects. Through our client survey data, we estimate that over 7,000 clients were able to keep their jobs due to our debt advice last year. When we look at our clients who have visited multiple times in the past few years, our advisers have helped gradually improve their surplus and reduce the number of people in a negative budget, despite repeated financial shocks.

Our data shows we have never been more needed, and yet the advice sector itself is not being adequately supported to deliver this critical help. We have helped hundreds of thousands of households to build financial buffers and access support that prevents them from reaching crisis point, but we can only do this if our resilience is also protected. The advice and charity sector is facing pressure on multiple fronts - from the impact of the rise in national insurance contributions, to the knock on impact of local authority cuts on our local offices, through to persistent flat funding that does not meet the scale of demand.

The benefits of advice can be seen not just through a societal lens but through a fiscal one. Our research shows that the advice we deliver directly saves government and public services around £681 million.[38]

At a time when the government is focussed on providing best value for taxpayers, whilst also raising living standards, they should look at how best to support and fund the advice sector. Alongside the policy changes outlined above, this would help people build up their resilience so that they have more of a financial buffer, and better access to support, to cope with any future shocks.

Endnotes

*All names and details have been anonymised

[1] The Coronavirus Job Retention Scheme final evaluation

[2] BBC News (2024) UK inflation rate -will prices keep rising?

[3] Debt clients are people who come to Citizens Advice for help managing their debts. Our advisers carry out a budget assessment with the client to help them make a sustainable repayment plan for their debts, and this assessment will include recording income and expenditure information. In 2019 and 2024 44,877 and 84,398 clients completed this process respectively.

[4] All polling figures quoted in this report are drawn from a nationally representative survey of UK adults conducted for Citizens Advice by Yonder Data Solutions. Total sample size 2,354. Fieldwork took place between 28th February and 2nd March 2025. People on disability benefits - defined as people on Personal Independence Payment, Universal Credit - Limited Capability for Work Related Activity element and Income based Employment and Support Allowance - were boosted to 511.

[5] For more information on the process of how we collect data on budget assessments, read our report from last year

[6] Whether or not an individual is in a negative budget or not is determined using the formula Surplus = Income.Total — Essential.Expenditure.Total. If the individual has a monthly surplus of less than zero they are classified as being in a negative budget. In 2019 36.7% of the clients who had a budget assessment were in a negative budget - in 2024 this rose to 48.6%.

[7] Using debt client data, we found that, for full-time workers, their trimmed mean (20%) average income went up by £528 between 2019 and 2024, but their trimmed mean (20%) essential expenditures went up by £522.

[8] BBC (2025), The seven bills due to go up in April

[9] Of our debt clients who had a budget assessment in 2024, we calculated the number who had a surplus of over £0 and less than or equal to £20. For this group, a price increase of £20 would push them to a surplus of between -£20 and £0 - therefore pushing them into a negative budget. This was 13% of all of our debt clients who received a budget assessment last year - equal to 5685 people.

[10] Calculated using internal Citizens Advice data. The number of people coming to us for debt advice is different to the number of people who need full budget assessments. Further details on our debt data can be found here.

[11] Kickstarting Economic Growth

[12] The Guardian (2025) How Labour's proposed benefits bill cuts could affect the most vulnerable

[13] Ministerial taskforce launched to kickstart work on child poverty strategy

[14] Quotes from advisers taken from 3 workshops carried out in summer 2024 with 44 frontline Citizens Advice advisers from across England and Wales. The workshops were conducted online and in person. The discussions focussed on negative budgets and debt. All names and details have been changed to ensure anonymity. Other quotes are taken from clients. All names for clients have also been changed to ensure anonymity.

[15] ONS, 2025 Private rent and house prices, UK: February 2025

[16] Citizens Advice, 2023 The impact of freezing Local Housing Allowance

[17] Citizens Advice, 2025 Citizens Advice Cost of Living dashboard, February 2025

[18] Of all the people in energy debt for whom we completed a budget assessment for in 2019, the average amount of energy debt per person was £835. This rose to £1412 per person in 2024. Further details on our latest debt data can be found here

[19] The Cornwall Insight predicts that prices are likely to fall slightly in July (from April), although it's too far out to predict accurately. Energy prices are extremely volatile and vulnerable to external shocks.

[20] Department for Energy Security and Net Zero, 2025 Expanding the Warm Home Discount Scheme, 2025 to 2026

[21] Citizens Advice, 2025 Frozen in place: Why the Government needs to move quicker to address energy affordability

[22] Issues with pay and entitlements are the biggest employment problem faced by our clients, with 1 in 3 (32%) of the more than 100,000 people who came to us for employment advice in 2024 needing help with issues like statutory sick pay, wages and payslips, holiday pay, and unlawful deductions.

[23] Citizens Advice, 2020 Tribunal trouble

[24] Citizens Advice, 2024 From rights to reality: Designing a Fair Work Agency that delivers for the most vulnerable workers

[25] Citizens Advice, 2023 In sickness and in health: Why Statutory Sick Pay needs further reform

[26] The Guardian, 2025 Labour unveils sick-pay guarantee for 1.3m lowest-paid workers

[27] Citizens Advice SSP Analysis

[28] Department for Work and Pensions, 2024 Household Support Fund 4 management information for 1 April 2023 to 31 March 2024

[29] Between 1st March 2024 and 28th February 2025, 59.7% of the people who came to us looking for support with the Household Support Fund were disabled or had a long-term health condition - 34,394 people.

[30] Citizens Advice, 2025 Short-sighted savings won’t fix health and disability benefits

[31] In 2019 we completed budget assessments for 44,877 people and in 2024 this rose to 84,398 people - a 88% increase. For all households with children we completed 19,472 and 38,701 budget assessments in 2019 and 2024 respectively - a 98.75% increase. For single parents alone we completed 12,038 and 26,756 budget assessments in 2019 and 2024 respectively - a 122% increase.

[32] Ministerial taskforce launched to kickstart work on child poverty strategy

[33] Joseph Rowntree Foundation Child poverty

[34] Department for Work and Pensions, 2024 Benefit cap: number of households capped to February 2024

[35] Of the 152,886 people we supported with Personal Independence Payment (PIP) in 2024, 43,575 had dependent children - 29%.

[36] We saw a 79% increase in the number of people coming to us with the top 6 most common cost of living issues between 2019 and 2024. These issues were Homelessness, Council tax arrears, Personal Independent Payment, Energy, Energy Debts and Charitable Support & Food Banks.

[37] Citizens Advice, 2023 We are Citizens Advice, we are the people’s champion